There are many people who wish to retire from work at an early age, which is a relatively nice idea for it allows one to have the ability to follow hobbies, spend more of his/her time with family, and lead carefree moments which do not encompass working for a specific employer all day long. Nevertheless, this goal is not easily attainable without the help of the establishing goals, preparation of a budget and adherence to it and making wise investments. To be able to afford this, it requires financial freedom, which is the secret to being able to retire early. It is possible to achieve the financial goals with regards to the lifestyle that an individual has. These will also make it fast for an individual to focus on such goals in this in depth article.

Also read – Roth IRA vs. Traditional IRA: Which is Right for You?

Understanding Financial Independence

What is Financial Independence?

Becoming financially independent means that a person has a reasonable amount of savings, investments and other revenue streams which enables him or her to live without an active income from work. A richer person is, however, not simply one who has more and more possessions, but rather one who is sufficiently protected that he can make choices — when, where, how and whether to work without worrying about funds. It is not a new concept as it also includes its corollary of retiring as soon as possible. Also known its abbreviation of FIRE (Financial Independence, Retire Early), it is an idea that many people cannot retire any more today than they have in the past on social security if one conforms to this principle. This curiosity about curiosity has been branded as a movement for returning to the budget surplus and planning to retire young.

The Importance of Goal Setting

The importance of gaining clarity on one’s financial goals comes before exploring the strategies. What amount would be required for early retirement? Any plans on the lifestyle during retirement? These questions are important since they help you calculate your “number,” or the amount of money that enables you to enjoy a lifestyle without having to earn an income.

It also means where you are setting the goals or targets; these will consider such things as inflation, healthcare and other market conditions that may prevail. As you set your goals, make sure that they are specific, measurable, attainable, realistic, and time-bound (SMART) as this will influence your financial choices and help you remain in the course of achieving your financial goals.

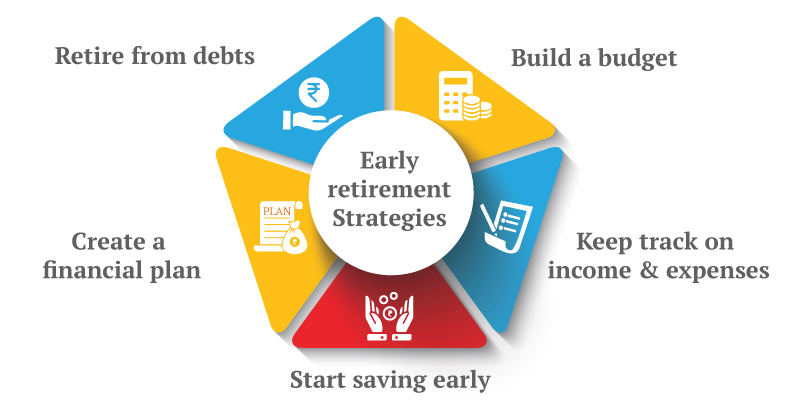

Strategies for Achieving Financial Independence

1. Live Below Your Means

Living beneath one’s earnings is among the foundations of attaining financial freedom. This means one spends less than the amount earned and there is no lifestyle creep which is when one increases the spending level in correspondence with an increase in income level. By living frugally, you would be capable of saving and investing most of your earnings, which would cut the time required to reach your financial independence.

Practical Tips:

- Budgeting: Get an accurate picture of where your money lion falls by establishing a comprehensive plan that highlights all your earnings and expenditures. You can adopt a few helpful tips such as the budgeting app or any other economic tool to record your patterns of expenditure and then eliminate unnecessary expenses.

- Reduce Discretionary Spending: Limit non-critical expenditures on food, entertainment, leisure, and other non-essentials. Separate needs from nice-to-haves

- Downsize: Relocate to a more affordable house or downgrade your vehicle in order to avoid huge outgoings such as mortgage payments, property taxes and insurance.

- Adopt a Minimalist Lifestyle: Practice minimalism by reducing the number of things you own but ensuring that what you have is meaningful to you. This may allow you to make some savings as well as tidy up the space.

2. Maximize Savings and Investments

The more you save, the sooner you will be able to achieve financial freedom. Seek to set aside a larger portion of your financial resources if you wish to retire at a younger age – 50% will be ideal. While this may mean foregoing certain pleasures in the short run, the rewards in the long run are immense.

Key Strategies:

- Automate Your Savings: Pay yourself first by establishing automatic withdrawals or transfers to your savings and investment facilities. This ensures that a portion of one’s income is always saved and this will grow over time.

- Tax-Advantaged Accounts: Take full advantages of one’s employers’ tax redeemable retirement plans such s 401(k)s, IRAs and HSAs. These plans are very much advantageous since taxes may have the adverse effect of diminishing the growth of savings.

- Employer Matching: When your employer provides a 401(k) match, ensure that you dedicate enough of your contribution to attain the full match. You consider it as free money and it enhances your savings rate.

- Investment Strategy: Choose a well diversified portfolio comprising of low-cost index funds, stocks as well as bonds. This is because, in the long run, investing in the stock market has generated higher profits as compared to other investments, hence, this becomes an important step in growing wealth.

3. Invest in Real Estate

The advantage of investing in properties is a great way towards financial independence. The rental use of these properties provides the investor with income as well as preparing & planning for retirement. Normally, there is no question that these properties will always increase in value thus increasing your wealth.

Consider These Options:

- Rental Properties: Buy investment properties which fetch positive rental income. This ensures that the gross rental income will be more than the operating costs of the property, including loans and upkeep.

- Real Estate Crowdfunding: Consider still investing in properties using real estate crowdfunding sites requiring less funds capital. This may be a good alternative for broadening the type of investments you have.

- House Hacking: This approach is buying multi family housing and living in one of the units while letting out the other units. The rental return on the rest of the units assists in servicing the home loan thereby reducing the housing expenditure enabling higher savings.

4. Diversify Your Income Streams

Taking a risk with just one source of income is impractical in cases where one loses their job or during the economic recession. That is why there is a need to supplement at least one income with other income sources to reduce such financial risks.

Income Diversification Ideas:

- Dividend Stocks: If you invest in stocks, go for those that pay dividends and earn you some extra income. You may decide to keep the money from dividends or buy more shares thereby increasing the overall returns of your investment.

- Side Hustles: Also, you will need to be looking for jobs to earn money. There are various types of online jobs in demand which involve conducting business activities hence helping to earn some money.

- Digital Products: Sell digital products like e-books, online courses, or apps. Such products can be a source of income with very little further active work required once completed.

- Real Estate Investments: Apart from the common rental properties, which people are gist about, there are regally developed Real Estate Investment Trusts (REITs) which will still give you exposure to real estate without the need to rent out an actual property.

5. Focus on High-Return Investments

To chuck up your job at a tender age, there is a level of income generation that is required invested above the normal inflation rate. Such investments are usually congregated on due to the great potential benefits that they offer. However, since these are high-return investments, growing your assets too quickly can be a problem also, hence risk management must be well thought out.

Investment Options:

- Stock Market: Long-term growth of an investor’s capital can therefore be accomplished through buying a wide range of stocks in a portfolio approach. Ensure that the risk is mitigated by including a combination of large-cap, mid-cap, and small-cap stocks, and also global stocks.

- Real Estate: We have however pointed out that real estate investments yield returns both from rent and appreciation within the course of time. Rental units and Real Estate Investment Trusts (REITS) seem to be the two most favoured investments to those who want to diversify.

- Peer-to-Peer Lending: Through their platforms, it is possible to lend money to people rather than to banks, earning interest on those loans that is much higher than the interest earned on an individual’s savings account. This is riskier, but it can give a better return on investment.

- Cryptocurrencies: Investing into cryptocurrencies such as Bitcoin and Ethereum entails making a high risk in hoping for reward, which can either come or not come. Only a manageable proportion of your portfolio should be allocated to cryptocurrencies.

6. Adopt a Frugal Mindset

Being frugal is not about starvation; it is simply about being resourceful and practicing smart spending decisions where worth comes before costs. By becoming a frugal person, one will such appreciable amount of money without having to compromise on lifestyle.

Frugal Living Tips:

- DIY Projects: Undertake do it yourself projects around the house, for repairs, cooking or even entertainment to cut costs. New skills are helpful and are a means to save money.

- Buy Used or Refurbished: Consider looking for used or ex-display furniture and electronics as well as second hand clothing. This helps you save a great deal of money while still enjoying the said goods.

- Couponing and Discounts: Cut back on grocery or shopping expenses by using coupons and apps which offer cash-back deals. Purchase non-perishable items in large quantities as often as possible.

- Travel Hacks: Save on vacations with the help of travel rewards, paying with credit card points, or travelling during the off peak seasons. When booking accommodation consider budget options, such as hostels or Airbnb, instead of overpriced hotels.

7. Leverage Tax Efficiency

Investment and savings can be adversely affected by taxes so the right approach is to use tax effective techniques. It is even said that when taxes are reduced, implementing financial independence could come quicker as your money multiplies.

Tax-Efficient Strategies:

- Tax-Advantaged Accounts: If you are able to, put as much as you can into tax privileged accounts such as 401 k’s, individual retirement accounts and health savings accounts. Most of these accounts will either enable the growth of your money without tax (tax-free) or tax-deferred depending on the type of account.

- Capital Gains Management: Maintain bonds and mutual funds for more than twelve months so that the gains are taxed at long term capital taxes which have lower rates than those for short term capital gains. Seek to shift taxable profits against taxable losses by means of tax loss harvesting.

- Roth IRA Conversions: In particular, look into converting your traditional IRA funds into a Roth IRA during low income earning years. Contributions to a Roth are made with after-tax dollars, and tax-free distributions of earnings can be useful if one anticipates moving into a higher tax bracket.

- Municipal Bonds: Investing in municipal bonds is a smart decision since most often than not, earnings from these forms of bonds are not taxed at the federal level, and sometimes at state & local levels too. This is often good for high income earners for it gives them income without taxes.

Planning for Early Retirement

1. Calculate Your Financial Independence Number

Your financial freedom number is an amount of money required to free you from work and still be able to enjoy life without working at an early age. The common one is the 25x rule, whereby one multiplies their yearly basically expenses by 25 to know how much of a pension fund they need to keep. This takes into tabs a 4 percent withdrawal rate which is on a 30-year retirement strategy considered to be in the safe zone.

Example: Where annual expenditures are $50000 this also means you will have to have saved $1.25m ($50000 x 25) to retire early.

Factors to Consider:

- Inflation: It’s also useful comparing the projected costs now with the costs, which could be expected in the future, say in 10 years. It is reasonable to plan for inflation in the long run, let’s assume 3% a year.

- Healthcare Costs: As you grow older, consider that you are likely to incur more health care costs. Try a long-term care insurance policy or save in a health savings account (HSA) for medical expenses in the future.

- Market Volatility: Be prepared for possible falls in the stock market by having a balanced portfolio and a cash buffer to sustain you through the difficult phase.

2. Develop a Withdrawal Strategy

Having reached your financially sound number, the next task will be to devise an optimal plan for withdrawals. The four percent rule is a popular recommendation, however, one should always reconsider their plans and modify them based on the situation and their spending requirements.

Withdrawal Strategies:

- The 4% Rule: Once you retire, use 4% of your retirement portfolio in its first year and subsequently adjust that with the inflation rate. This particular strategy ensures the portfolio is sufficient for at least a time span of 30 years.

- Variable Percentage Withdrawal: With regards to withdrawal percentages, they take into account how the investment performs. If one year is worse than the other, withdraw less that year so that savings last longer.

- Bucketing Strategy: Use different “buckets” for your portfolio according to the anticipation of the funds usage. For example, retain between 3-5 years of your living expenses in cash or cash equivalents, while the remaining portion is invested in higher risk assets.

3. Plan for Healthcare

Retirement is marked by several other expenses as well with healthcare topping the list, especially where retirement is taken before the age of 65 when one can qualify for the Medicare age. It is very important to take healthcare costs into consideration and think of strategies for acquiring health insurance.

Healthcare Planning Tips:

- Health Insurance: In case one is taking early retirement, it would be paramount to find ways to get health insurance till one reaches 65 when she/he can get Medicare insurance. Choices are COBRA, individual market policy or spouse plan.

- Health Savings Account (HSA): Make HSA contributions on behalf of the working individual with the purpose of generating a tax free account in retirement meant for medical spending. Prairie’s triple tax advantage of HSAs is that contributions are tax deductible, earnings are tax free and qualified medical expense provisions are tax free.

- Long-Term Care Insurance: Consider purchasing long-term care insurance which will enable you to pay for nursing home care, assisted living or even in-home care. In the absence of strategies to stave off such expenses, retirement funds can thin out rather quickly.

4. Consider Part-Time Work

If this is your first time retiring early, you don’t suppose that you won’t find any employment again right? Many of the early retirees tend to take on some form of work or creative activities that generate some additional income. It can allow your retirement funds to last longer and help you remain active and happy during retirement.

Benefits of Part-Time Work:

- Supplemental Income: Some retired people will still work on a part-time basis so that daily needs will be taken care of without any drawing down of retirement funds.

- Social Interaction: Taking a part time job can also provide social interactions even if they are few and provide direction which are important when not working.

- Health Benefits: A few part-time positions even provide health coverage which is truly useful if you are contemplating early retirement.

Conclusion

Early or premature retirement and attaining the status of being free from the financial pressures of work isn’t easy, and yet very achievable. It is, however, going to take time and rigorous planning, proper sacrifices, and wise investment decisions. Making use of the ideas discussed above of living below one’s means, saving as much as possible and investing that money into various assets, creating numerous sources of income, and preparing for the worst is that there is hope for best and worst. Recall that the path to attaining wealth and physical wellbeing is more of a marathon than a short race. It is important to remain focused on the vision, keep checking the goal, change tracks where it is deemed necessary. It will be possible to retire rather early with the right ideas and hard work.